By Michel Brekelmans

While Chinese manufacturing is yet to fully embrace industrial automation, forward-thinking businesses and players are positioning themselves to take advantage of the potential growth opportunities of Industry 4.0, or the Internet of Things.

What is Industry 4.0?

The fourth industrial revolution is the move toward advanced industrial devices, systems and services that will deliver less costly, more efficient use of assets and increase business value. These outcomes are achieved by analyzing data to improve decision making about the use of resources. Industry 4.0 solutions will typically link the physical and cyber world through cyber-physical systems (CPS). Examples of CPS-driven solutions are self-learning robots, predictive maintenance, self-reconfiguring machines, and smart environment recognition.

Like the previous three industrial revolutions, Industry 4.0 heralds a new stage in industrial manufacturing which will disrupt existing markets and competition and demand new requirements of businesses’ staff and infrastructure.

Toward Industry 4.0: China’s growth potential

Before China can step into the fourth industrial revolution, it needs to transform its automation. China needs to fully implement automation in production processes, including data collection and analysis, which makes China an attractive market for industrial automation businesses.

Penetration rates of industrial automation in China lag behind other developed markets. The low rates of industrial robot density in China compared to Korea, Japan, Germany and the United States offer growth potential for prospective industrial automation market companies.

The growth potential for industrial automation in China is supported by:

- Chinese government measures to shift the manufacturing focus toward technology-intensive industries by promoting the use of robotics. In addition to providing loans and tax incentives to high-tech manufacturing industries, China’s 12th Five-Year Plan (2011 to 2015) targeted the intelligent manufacturing equipment industry. The 13th Five-Year Plan (2016-2020) has set a target of establishing a complete system and industry chain for intelligent manufacturing equipment with a total market value of more than RMB 300 billion. This will increase support for industrial and service robotics and drive the technology and high-end manufacturing industries. The Made in China 2025 plan has a 10-year goal that emphasizes innovation. Looking ahead to 2049, the Chinese Government’s long term plan is to transform China into a leading manufacturing power to rival Germany, Japan and USA.

- Rapidly rising labor costs. Dramatic increases in labor costs pressured many manufacturers to move operations to lower-cost countries (eg, Vietnam) or look at ways in which they can reduce their dependency on manual labor. This will drive demand for industrial automation in manufacturing.

- Labor Productivity Goals. Chinese manufacturers are under similar pressure to increase labor productivity to stay competitive. An assessment of China labor productivity metrics shows industrial sector workers leading the way compared to workers in the Agriculture and Services sectors. As manufacturers look for different solutions to continue to improve labor productivity, the advantages offered by industrial robotics will be on their radar.

Increased capacity and capabilities of international and domestic players. Multinational companies and domestic manufacturers are investing in (and generating) increased capacity and capabilities in China and this will assist in driving market growth for industrial robotics. These investments in manufacturing facilities draw attention to the limited number of domestic robotic manufacturers in China (though there are several planned domestic industrial robotics bases with the target of increasing capacity and capabilities). Automation suppliers are actively promoting their solutions through marketing and training, which raises awareness and increases demand.

China’s Growing Market for Industrial Robotics

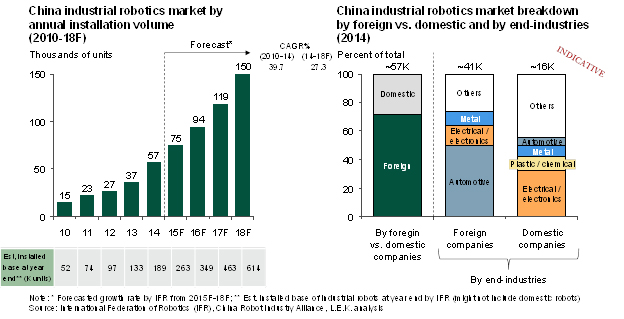

China’s industrial robotics market has grown significantly to become one of the major global markets. As demonstrated by Figure 2, annual installation volume increased steadily from 15,000 units in 2010 to 57,000 units in 2014. Further increases are forecast to 2018. Figure 2 also reflects the dominance of foreign players in China’s industrial robotics industry, with more than 70% market share. However, a breakdown of foreign and domestic companies’ market shares according to end-industry reveals some interesting trends. Multinational companies have a strong presence in the automotive industry, whereas domestic players are stronger in the electrical/electronics sector.

Domestic players face a number of challenges in securing a greater share of China’s industrial robotics market, including:

- Limited scale in manufacturing (only very few companies can manufacture over 100 units per year);

- A technology gap compared to multinational companies’ robots (eg, higher frequency of manufacturing errors and more maintenance requirements for domestic robots);

- High costs for core components (domestic players need to purchase core components from multinational company manufacturers);

- A lack of research and development and innovation (which reduces domestic players’ competitiveness); and

- High software development costs.

Recently, Chinese home appliance giant, Midea, announced plans to acquire a 49 percent stake a leading German industrial automation company, KUKA, for 4.5 billion euros. KUKA is one of the largest manufacturers of industrial robots with strong presence in automotive industry, which accounts for half of its revenue in 2015. Midea plans to leverage KUKA’s capability and experience to enter the industrial robotics industry and so become one of the overnight leaders in China.

Taking the lead in industrial automation: China’s automotive sector

The most advanced Chinese industrial automation sector is the automotive industry. A variety of applications within the Chinese automotive market (eg, welding, grinding, assembly and dispensing) have been automated with flexible robotics systems. Demand for automation in the Chinese automotive sector is expected to grow at around 7% per year through to 2019 (though this is slower than other market segments due to higher existing penetration). Robotic density in the automotive sector rose by 29% between 2011 and 2013 on the back of increasing labor costs and government subsidies geared towards creating safer workplaces

Within the Chinese automotive end market, there are various entry points for robotic systems integrators across the manufacturing value chain. Highly fragmented, smaller systems integrators may enter the market to provide solutions for Tier 2/3 suppliers, while systems integrators (some with building capabilities) and robotic line builders may service Tier 1 suppliers or original equipment manufacturers (‘OEMs’). These possible entry points all have varying levels of customer concentration and growth outlooks. For example, OEMs represent the largest segment for robotic systems in China, but they are already significantly automated and tend to have entrenched relationships with line builders. For Tier 1 suppliers the assembly processes of sub-components are not extensively automated, but as labor cost pressures and quality demands from OEMs grow, robotic adoption should increase. For example, automated laser welding systems have recently started replacing older spot and arc welding systems (particularly among auto seat suppliers). And buffing and grinding applications for components such as transmission boxes are likely to grow as well.

When it comes to hiring a systems integrator in China’s automotive sector, the primary differentiator for OEMs is technical background and capabilities, which minimize project risks. On the other hand, component suppliers – particularly domestic suppliers – are primarily cost-conscious in approach. Secondary considerations in selecting a systems integrator are prior project experience as well as track record and reputation.

Significant entry barriers exist in the form of preferred vendor lists for OEMs and foreign suppliers, technical/specialization requirements for OEM’s, and the prevalence of low-cost domestic systems integrators who can meet suppliers’ requirements. Apart from automotive OEMs, competitive intensity is relatively high due to less complex robotic systems demands and high fragmentation.

Conclusions: Lessons to be learned from the automation of China’s automotive sector

China’s automotive industry demonstrates that China’s manufacturing sector will embrace industrial automation sooner rather than later. Leading, agile players will position themselves for the opportunities on offer as the fourth industrial revolution (‘Industry 4.0’) and the ‘Internet of Things’ (‘IoT’) take hold in China. Looking ahead, it is the combination of connected machines and big data analytics which will cut manufacturing and service costs. The greatest benefits delivered by the IoT will be applications that capture and analyze the vast amount of data generated by automated systems. Future investment will focus on developing applications to add value to the industry-specific use of industrial robotic systems.

For those players wanting to take advantage of the opportunities from a rapidly-automating Chinese manufacturing sector, an effective IoT strategy is crucial. There are a number of important guiding principles to develop an effective strategy. In essence, an organization should contemplate what it currently does and what it wants to achieve, assess the options for building an IoT solution, and determine the related organizational implications.

About the author: Michel Brekelmans is a managing director and co-head of L.E.K. Consulting’s China practice based in Shanghai. L.E.K. Consulting is a global management consulting firm that uses deep industry expertise and rigorous analysis to help business leaders achieve practical results with real impact. For more information, contact [email protected].